Wall Street is drunk on server racks. When Dell’s shares jumped 35% on the back of "AI fervor," the financial press rolled out the usual copy-paste narratives about a hardware renaissance. They looked at the massive backlog of Nvidia-powered servers and mistook assembly line volume for strategic dominance.

They are celebrating a middleman for moving boxes.

The mainstream consensus says Dell is a primary beneficiary of the artificial intelligence boom because enterprise clients need infrastructure. The reality is far more brutal. Dell is running a low-margin commodity business dressed up in a trillion-dollar buzzword. They are taking massive capital risks to aggregate components they don't control, selling to hyperscalers who will drop them the second supply chains ease, and operating on margins that would make a software engineer weep.

The Assembly Line Illusion

Let’s dismantle the core premise of the bull case. The narrative assumes that because a company sells the infrastructure required for AI, it commands a premium position in the tech stack. This conflates volume with value capture.

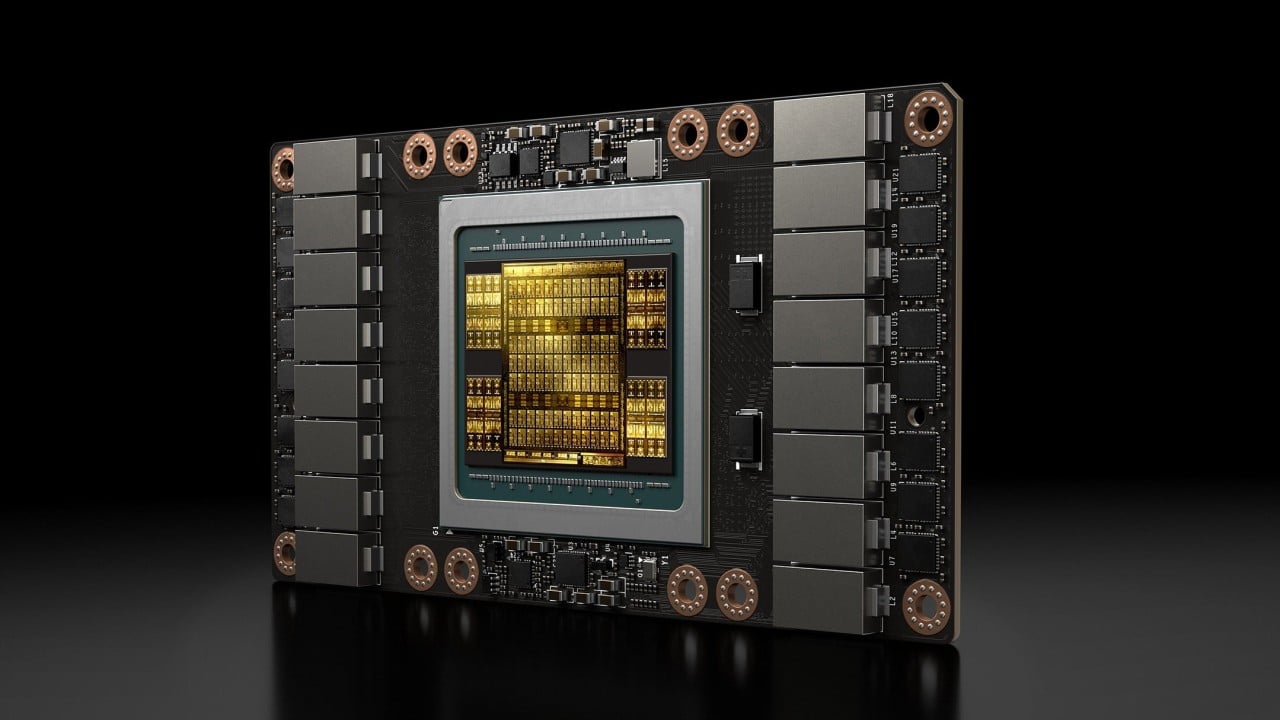

Dell does not manufacture the H100, B200, or any of the silicon driving this cycle. Nvidia does. Dell does not own the proprietary architectural designs or the software ecosystem like CUDA. They buy chips from Santa Clara, plug them into proprietary metal chassis with power supplies and fans, and ship them out.

In hardware, the entity that owns the intellectual property captures the rent. The entity that screws the IP into a motherboard captures the crumbs.

I have watched enterprise infrastructure cycles play out for two decades. In every single wave—from the early blade server boom to the hyper-converged infrastructure craze—the story ends the same way. When a specific component is scarce, the system integrator who can secure allocation looks like a genius. Their revenue skyrockets. Investors mistake supply-chain favoritism for a structural competitive advantage.

But allocation is temporary. Capacity catches up. When it does, the premium disappears, and you are left looking at the underlying unit economics of a box-shipper.

The Brutal Reality of Server Margins

Look closely at the financial statements, not the press releases. Historically, Dell’s Infrastructure Solutions Group operates on operating margins hovering in the high single digits or low teens. When you inject hyper-expensive Nvidia GPUs into the mix, the top-line revenue explodes because a single server now costs as much as a small house.

But your gross margin percentage compresses.

Why? Because Nvidia holds all the pricing power. If a server costs $300,000 and the GPUs inside account for $250,000 of that cost, Dell is passing through Nvidia’s massive gross margin while taking a razor-thin markup on the remaining components. They are absorbing massive working capital risk—carrying billions in inventory and accounts receivable—to book low-margin revenue.

[Nvidia: Owns IP & IP Ecosystem] ---> High Margins (75%+)

[Dell: Assembles & Dispatches] ---> Low Margins (<15%)

If you are celebrating a 35% stock pop based on this dynamic, you don't understand the difference between high-quality recurring revenue and low-quality capital-intensive pass-throughs.

The Hyperscaler Trap

The second pillar of the lazy consensus is that enterprise demand is insatiable and permanent. This ignores the customer mix.

The initial surge in high-end AI server orders does not come from Main Street banks or regional healthcare providers buying clusters for their local data centers. It comes from tier-two cloud providers, specialized AI hosters, and massive hyperscalers who are desperate for compute capacity right now because they cannot get enough direct allocation from chipmakers.

This is a transactional relationship, not an ecosystem lock-in.

- Hyperscalers prefer custom silicon: Google has the TPU. Amazon has Trainium and Inferentia. Microsoft has Maia. Meta is building its own chips. The biggest spenders in tech do not want to buy standard x86 or standard PCIe server architectures from legacy OEMs over the long term. They are using commercial off-the-shelf hardware as a stopgap measure to satisfy immediate demand while they scale their internal silicon programs.

- Enterprise adoption is lagging: True enterprise AI deployments are stalled in pilot purgatory. Companies are realizing that fine-tuning an open-source model requires massive data engineering work, clean data pipelines, and strict compliance frameworks. They do not need twenty liquid-cooled AI servers sitting in a corporate closet today. They need data cleanup.

When the specialized cloud hosters finish building out their initial footprint, and when the hyperscalers bring their own silicon online at scale, the order book for expensive, margin-dilutive AI servers will normalize overnight.

Dismantling the "People Also Ask" Flawed Premises

The questions retail investors ask reveal how deeply the marketing narrative has penetrated the public consciousness. Let’s address the most common misconceptions directly.

"Is Dell a better AI investment than software companies?"

This question assumes that physical infrastructure is safer because it is tangible. It is the exact opposite.

Software companies have high upfront development costs but near-zero marginal costs of distribution. Once an AI software platform scales, every dollar of new revenue drops straight to the bottom line. Dell faces a physical bottleneck. To sell another server, they must buy another chip, secure another power supply, ship another heavy box, and provide field support.

Investing in hardware infrastructure at the peak of a build cycle, while avoiding the software layer that utilizes that infrastructure, is like investing in the shovel manufacturers during a gold rush after the gold fields have already been claimed by a few mega-corporations.

"Won't sovereign AI and national data centers protect Dell's growth?"

The argument here is that nation-states want localized AI clusters for national security reasons, and they will turn to trusted legacy brands like Dell to build them.

While nation-states are building localized clouds, they are not writing blank checks for brand names. They are looking for cost efficiency and absolute control over the hardware design. This opens the door for Original Design Manufacturers (ODMs) from Taiwan and Quanta-style white-box manufacturers who build directly to specification without the enterprise sales markup. The legacy salesforce model that served Dell so well in the PC era is an expensive liability when competing for massive, centralized government infrastructure contracts.

The Sovereign Danger of Direct Access

Let’s run a thought experiment. Imagine a scenario where Nvidia decides to expand its own cloud offering, DGX Cloud, to sell compute directly to enterprises.

In this world, Nvidia hosts the hardware in co-location facilities, provides the software layer, and bypasses the traditional server OEMs entirely. They have already started doing this. They realize that to protect their massive margins, they must control the distribution of the compute, not just the sale of the silicon.

Where does that leave the traditional hardware maker?

It reduces them to a niche player catering to the tail end of the market—companies too small or too paranoid to move to the cloud, who lack the internal engineering talent to build their own systems. That is a real business, but it is not a high-growth tech darling worth a massive earnings multiple extension.

The Real Winner of the Hardware Boom is Not Who You Think

If you want to understand where the real value is being captured in the physical layer of artificial intelligence, stop looking at the logo on the front of the server box. Look at what happens when you put ten thousand of those boxes in a single building.

They pull massive amounts of electricity. They generate terrifying amounts of heat.

The true, non-obvious bottlenecks in infrastructure are power generation, electrical grid components, and advanced liquid cooling systems at the facility level. Companies that control the electrical transformers, the industrial switchgear, and the specialized chillers have massive pricing power and immense moats. They cannot be easily bypassed by custom silicon. Their products cannot be replaced by a software update.

Dell is forced to source these cooling components from third parties to bundle into their systems, adding another layer of cost to an already squeezed margin profile.

The Actionable Verdict for Allocators

Stop chasing the trailing momentum of hardware earnings reports that reflect past supply chain allocations rather than future structural advantages.

If you hold legacy hardware stocks because of an "AI re-rating," lock in those gains before the capital expenditure priorities of the hyperscalers shift from frantic capacity accumulation to rigorous cost optimization.

If you must invest in the physical layer of tech, look for the unsexy, non-commodity monopolies:

- Grid infrastructure and power management firms that own the physical bottleneck of data center expansion.

- Specialized thermal management engineering companies whose intellectual property is mandatory for high-density compute, regardless of who wins the chip or server wars.

The 35% surge in valuation is not a sign of a new tech titan emerging; it is the final, loudest gasp of a legacy business model getting a temporary adrenaline shot from a macro cycle it does not control. Turn off the financial news, look at the margin compression, and step away from the hype machine.